Did Anthropic and OpenAI Just Make Your Tech Services Business More Valuable?

Highlights:

Anthropic and OpenAI launched PE-backed services ventures within a week of each other, committing a combined $5.5 billion and signalling that human-led AI implementation is where the next wave of enterprise value will be created.

Both ventures will need to acquire to scale. The structural conflicts built into the lab-owned services arms mean independent, people-led businesses are better placed to serve clients over the long term.

A new and well-capitalised class of buyer has entered the mid-market tech services space, and acquirers are likely to accelerate their own activity in response, creating upward pressure on valuations across the sector.

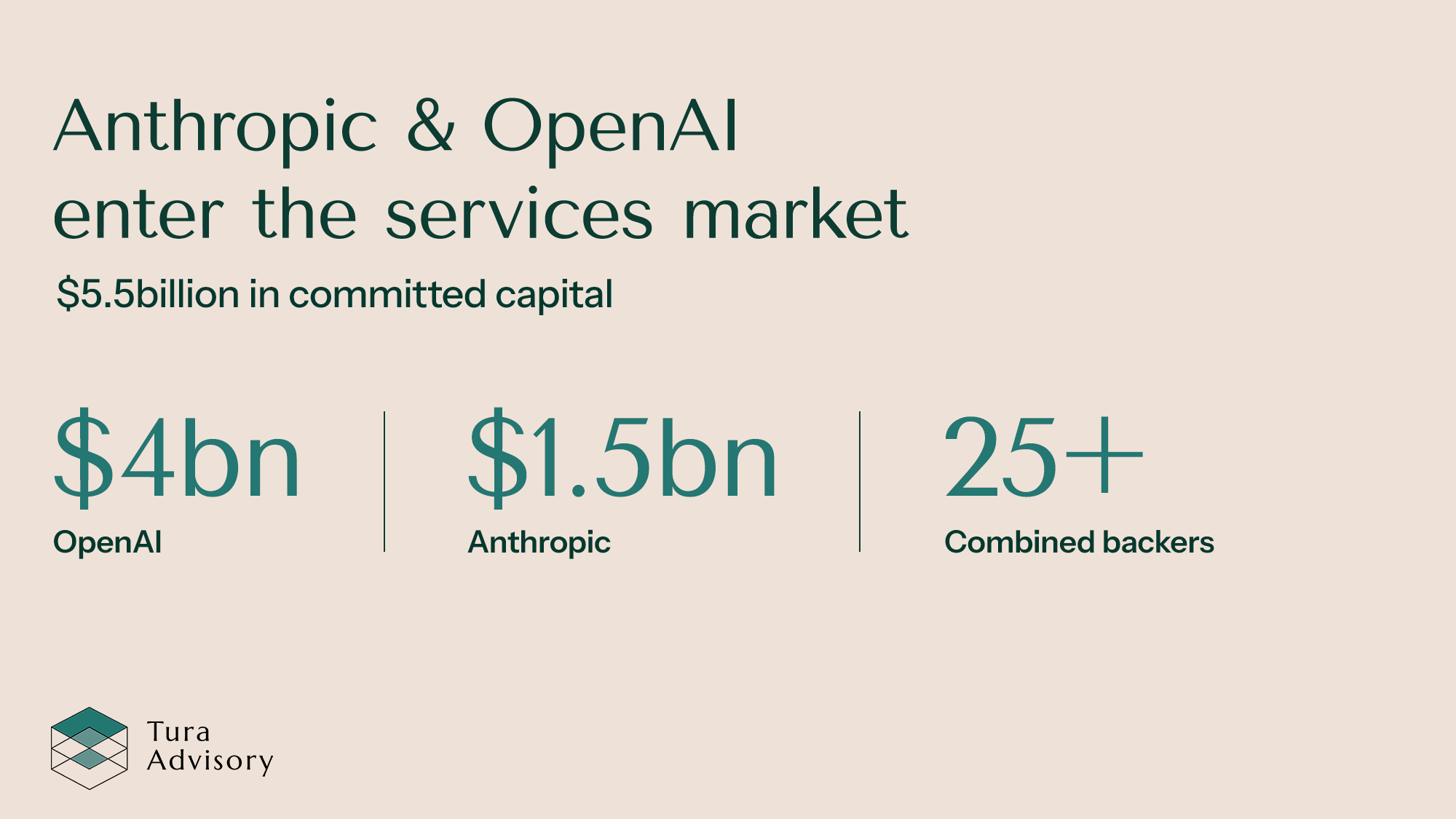

In May 2026, Anthropic and OpenAI both launched PE-backed services ventures within a week of each other, committing a combined $5.5 billion. Backers include Blackstone, Hellman & Friedman, Goldman Sachs, TPG, Advent, Bain Capital and Brookfield. Coverage has focused on deal size and the names attached, while the M&A implications of these announcements have received less attention than they deserve.

Both ventures are built on the same underlying logic: organisations across every sector are finding that access to powerful models doesn't automatically translate into operational value. Somebody needs to go in, understand how the business runs, redesign the workflows, manage the change and make the technology stick. That work is human. It requires relationships, judgement and sustained delivery capability. By structuring these ventures around major PE firms, both companies have also created a motivated distribution channel of investors with direct financial interest in seeing their portfolio companies adopt and embed the platform.

That combination of committed capital, scale ambition and PE-backed distribution has direct implications for the value of people-based tech services businesses. Both ventures will need to acquire at pace to build the delivery capability their investors expect. Established acquirers will accelerate their own activity in response. The businesses that benefit most will be those that understand what they have built and are ready when the conversation arrives. This article sets out why.

Acquisitions are inevitable

Both Anthropic and OpenAI have been explicit about the operating model their ventures will use. Anthropic's announcement described applied AI engineers working "alongside the firm's engineering team to identify where Claude can have the most impact, build custom solutions, and support customers over the long term." OpenAI's Chief Revenue Officer Denise Dresser stated: "AI is becoming capable of doing increasingly meaningful work inside organisations. The challenge now is helping companies integrate these systems into the infrastructure and workflows that power their businesses."

OpenAI's response to that challenge centres on Forward Deployed Engineers (FDEs) - specialists embedded directly inside client organisations to redesign workflows, connect AI to business data and build systems that work in day-to-day operations. This delivery model requires people with genuine implementation track records, and building that capacity through hiring alone can take years. When capital is committed, and investors expect returns at the pace that $4 billion demands, the established route to scale has always been acquisition.

Both ventures have announced that acquisitions are central to their growth strategy, and OpenAI confirmed its first alongside the DeployCo launch. Tomoro, a London-headquartered applied AI consultancy founded in 2023, will bring approximately 150 experienced FDEs and deployment specialists to DeployCo from day one. Tomoro's client base includes Fidelity International, Virgin Atlantic, Tesco, the NBA and Red Bull - established enterprise relationships that take years to build and cannot be replicated through recruitment alone.

Anthropic followed with its own first acquisition. Fractional AI, a San Francisco-based applied AI consultancy founded in 2024, will serve as the founding operational centrepiece of Anthropic's new venture, bringing a team of engineers built specifically to embed AI into enterprise workflows.

Two acquisitions within weeks of the announcements. Both ventures have signalled there will be more, each one setting a new reference point for what AI-native services businesses in this market are worth.

Allie K. Miller, a widely followed voice in enterprise AI, noted in the days following the announcements: "The most expensive mistake in enterprise AI right now is treating FDEs as your whole transformation plan." Engineers can deploy technology, but changing the culture, behaviours and working practices of an organisation is a different kind of work. "It's the combination of tech and people enablement and process reinvention," Miller wrote, "that compounds into actual business outcomes." The FDE model covers the technical half of that equation. The other half, sitting with leadership, understanding the business deeply, and driving the organisational change that makes the technology stick, is what people-led services businesses do. That makes them not just attractive acquisition targets, but necessary ones.

Independent businesses hold a structural advantage

Anthropic's announcement acknowledges that its Claude Partner Network, which includes Accenture, Deloitte and PwC, remains central to how it reaches large enterprises. Embedding a proprietary services arm into that same ecosystem puts it in direct competition with the very partners it depends on. OpenAI faces the same tension with its own partner and reseller network. Both ventures have, in effect, launched businesses that compete with the distribution channels they cannot afford to lose.

A services arm owned by an AI company has a structural incentive to maximise usage of its own models, regardless of whether that represents the most efficient or appropriate solution for a given client. Truly vendor-agnostic advice that builds long-term client trust is difficult to deliver when the adviser's parent company is also the technology provider. That conflict drives clients toward independent businesses that can offer impartial guidance, building the sticky, long-term relationships that acquirers value most highly when assessing a business.

What this means for mid-market valuations

Two forces are now in motion simultaneously, and both point in the same direction for founders of mid-market tech services businesses.

The first is direct. Both ventures have committed capital, PE-backed investors are expecting returns, and the delivery model requires acquired capability to scale. Founder-managed businesses are well placed to benefit from the acquisition wave that follows. They tend to be smaller, more digestible businesses that are more likely to carry the specialist capability and focused service offering these ventures are looking for, rather than a larger business that comes with 80% of services they have no interest in adopting. The commercial profile, the established client relationships and the AI implementation track record all support a valuation conversation. A new and well-capitalised class of buyer is in the market, and founder-managed businesses are a natural fit for what they need.

The second is indirect. Established players such as Accenture, IBM, Capgemini and Cognizant are unlikely to watch well-funded competitors build captive delivery networks across hundreds of PE portfolio companies without responding. The competitive pressure alone will accelerate their own activity in AI-native services. As Megabuyte noted in a recent analysis of the announcement, shared with its subscriber base, further acquisition activity "is likely and will set new watermarks in terms of AI-native services company valuations."

More buyers. More competition for the right assets. Upward pressure on valuations across the sector.

The businesses best placed to benefit will already be demonstrably implementing and supporting AI transformation at enterprise scale. The good news is that for many mid-market tech services businesses, that foundation already exists. The relationships, skills and expertise built through years of digital transformation work are directly transferable. The businesses that recognise that and are actively applying it to AI transformation - with real client outcomes to support it - are the ones that will attract the most serious interest off the back of this market shift.

The verdict

Did Anthropic and OpenAI just make your tech services business more valuable? It looks positive.

The announcements are already reshaping the M&A landscape for mid-market tech services businesses. A new and well-capitalised class of buyer has entered the market with both the capital and the strategic need to acquire focused, people-led businesses at pace. Established acquirers, unwilling to cede ground, will most likely accelerate their own activity in response.

At the same time, the structural conflicts built into these ventures mean that founder-led businesses with genuine, vendor-agnostic delivery capability are businesses the market cannot replicate. That will put them in strong standing when valuations are being discussed.

In a market that’s not been short of uncertainty, this is a reason to feel more bullish about exit prospects. The opportunity for people-led, founder-driven tech services businesses just got better. The businesses that benefit most will be those that are ready to take advantage of it.

If you want to understand what your business could be worth in this market, speak to the Tura Advisory team.