Therapeutic Specialisation: The New Premium In CRO Deal Making

Highlights:

The global CRO services market is projected to grow from $93 billion in 2026 to $140 billion by 2031, with acquisition activity concentrating in oncology, rare disease and CNS.

Buyers are acquiring therapeutic depth rather than building it, as demonstrated by Worldwide Clinical Trials' acquisition of Catalyst Clinical Research in February 2026.

Specialist CROs in high-growth therapeutic areas are commanding premium valuations, but only where specialisation is genuine, documented and distributed across the organisation.

In diligence, buyers distinguish businesses where specialist capability is institutional from those where it is individual or merely positioned.

The global CRO (contract research organisation) market is projected to grow in value from $93 billion in 2026 towards $140 billion by 2031. As that growth accelerates, acquirers in healthcare and life sciences are competing to secure specialist capability ahead of demand - deep expertise, established site and investigator networks, and a track record in specific therapeutic areas.

Recent acquisition activity in the CRO sector reflects this directly. Buyers are not acquiring scale - they are acquiring embedded capability in therapeutic areas where clinical complexity is highest and demand is growing fastest. The deals being done demonstrate that acquirers will pay a premium for genuine specialist depth, but the scrutiny applied in diligence is significant. Businesses where specialisation is documented and distributed across the organisation are achieving materially different outcomes from those where it exists only in positioning.

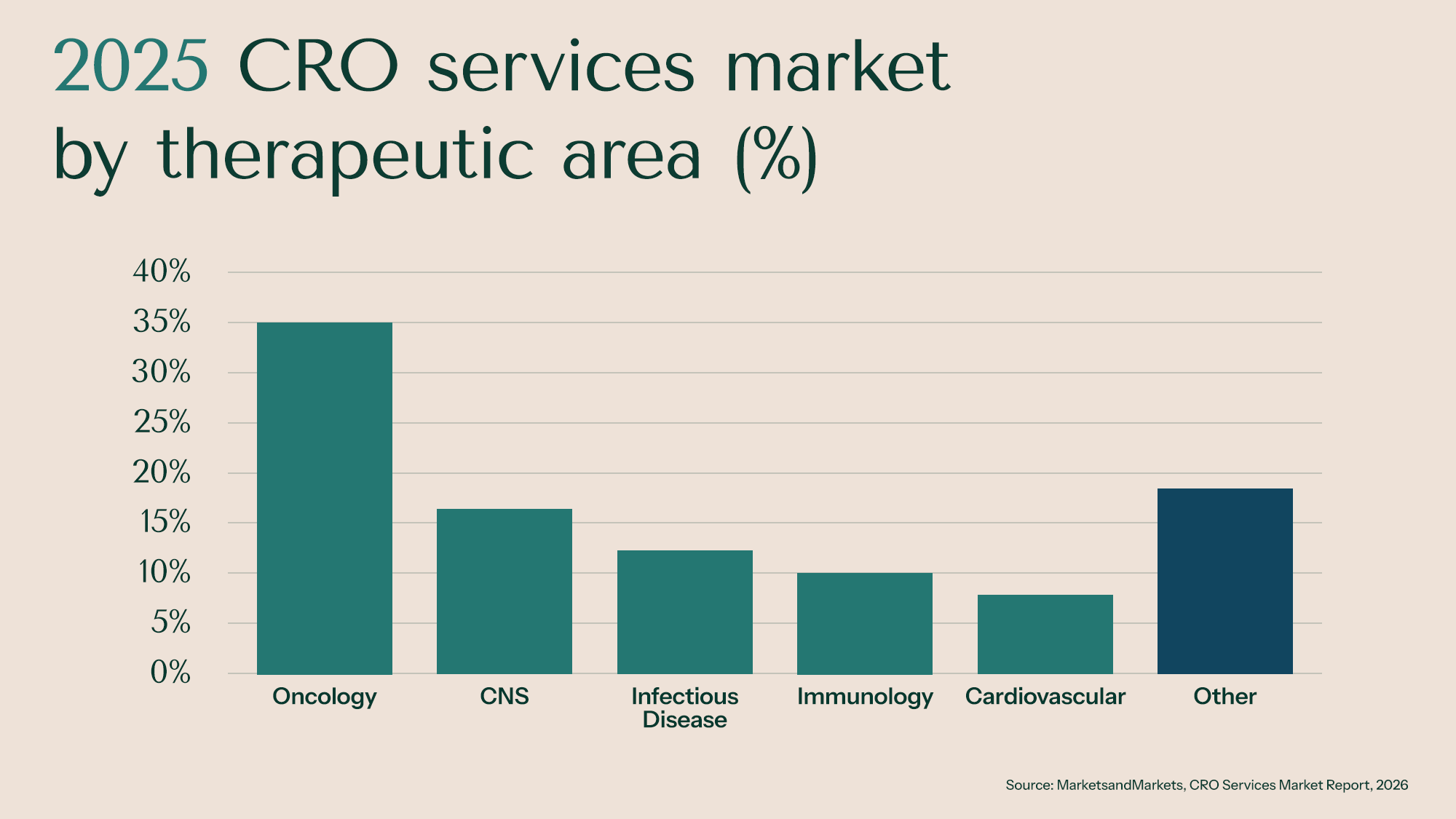

Trial volume is concentrating in oncology, rare disease and CNS

Three areas are driving concentration of demand in CRO acquisition: oncology, rare disease and CNS (central nervous system) disorders.

Oncology is the largest therapeutic area in clinical development, accounting for 35.5% of the global CRO services market. Cancer remains the most innovation-intensive disease area, with expanding drug approvals, increasingly complex trial designs, and a shift toward precision medicine and biomarker-driven protocols that require deep specialist knowledge to execute.

The rare disease segment is growing rapidly, with the rare disease CRO market forecast to expand at a CAGR of 8.18% from 2026 to 2031. In the wider rare disease treatment market, that figure rises to around 11.6% over the same period, reflecting the scale of investment flowing into this area. Half of novel drugs approved by the FDA in 2025 (23 of 46) received orphan drug designation for rare diseases, and the average time to diagnosis has fallen from seven years in 2015 to under five years in 2025, meaningfully enlarging the trial-eligible patient population.

CNS disorders represent a third area of concentrated growth, forecast to expand at the fastest CAGR of any therapeutic segment through 2034. Alongside cell and gene therapy - where more than 2,500 active investigational new drug (IND) applications were on file with the FDA in 2023-24 - these are the areas where clinical complexity is highest, and the premium for genuine specialist expertise is most pronounced.

CROs with deep expertise in these areas have the most structurally defensible client relationships. Sponsors running oncology or rare disease programmes select CROs based on principal investigator (PI) networks, site activation speed and regulatory track record. Those are not capabilities that can be reproduced quickly through marketing investment. That structural depth, which has been built over years of trial delivery in complex indications, is what acquirers are targeting and underpins premium valuation in the current market.

The acquisition of Catalyst Clinical Research

Worldwide Clinical Trials, a global CRO backed by Kohlberg, completed its acquisition of Catalyst Clinical Research in February 2026. Catalyst is a specialist oncology CRO focused on early-phase trials and functional service provider (FSP) delivery. The deal is a demonstrable example of how this buyer interest is playing out in the current market.

Catalyst's early-phase oncology expertise complemented Worldwide's late-phase strength, while the FSP model and biometrics capability added recurring revenue and commercial breadth. The deal brought first-in-human and Phase I/II expertise, an established investigator network, and more predictable revenue than project-by-project delivery.

Speaking at completion, Worldwide CEO Alistair Macdonald said, “[The deal] expands our reach into earlier phase oncology, adds targeted FSP and biometrics capabilities, and accelerates our technology platforms, allowing us to better support customers across the full development lifecycle with greater speed, flexibility, and transparency."

The deal sits within a broader pattern. Julius Clinical's merger with Peachtree BioResearch Solutions added CNS expertise. Link Medical AS acquired CRST for first-in-human capability. ICON's acquisition of KCR in August 2024 strengthened its Central and Eastern European site network and FSP capability across multiple therapeutic areas. In each case, the acquirer was paying for something specific and defensible.

What buyers scrutinise in diligence

Genuine therapeutic specialisation commands a premium, but buyers are increasingly sophisticated at distinguishing between businesses where it is real, and those where it is positioned.

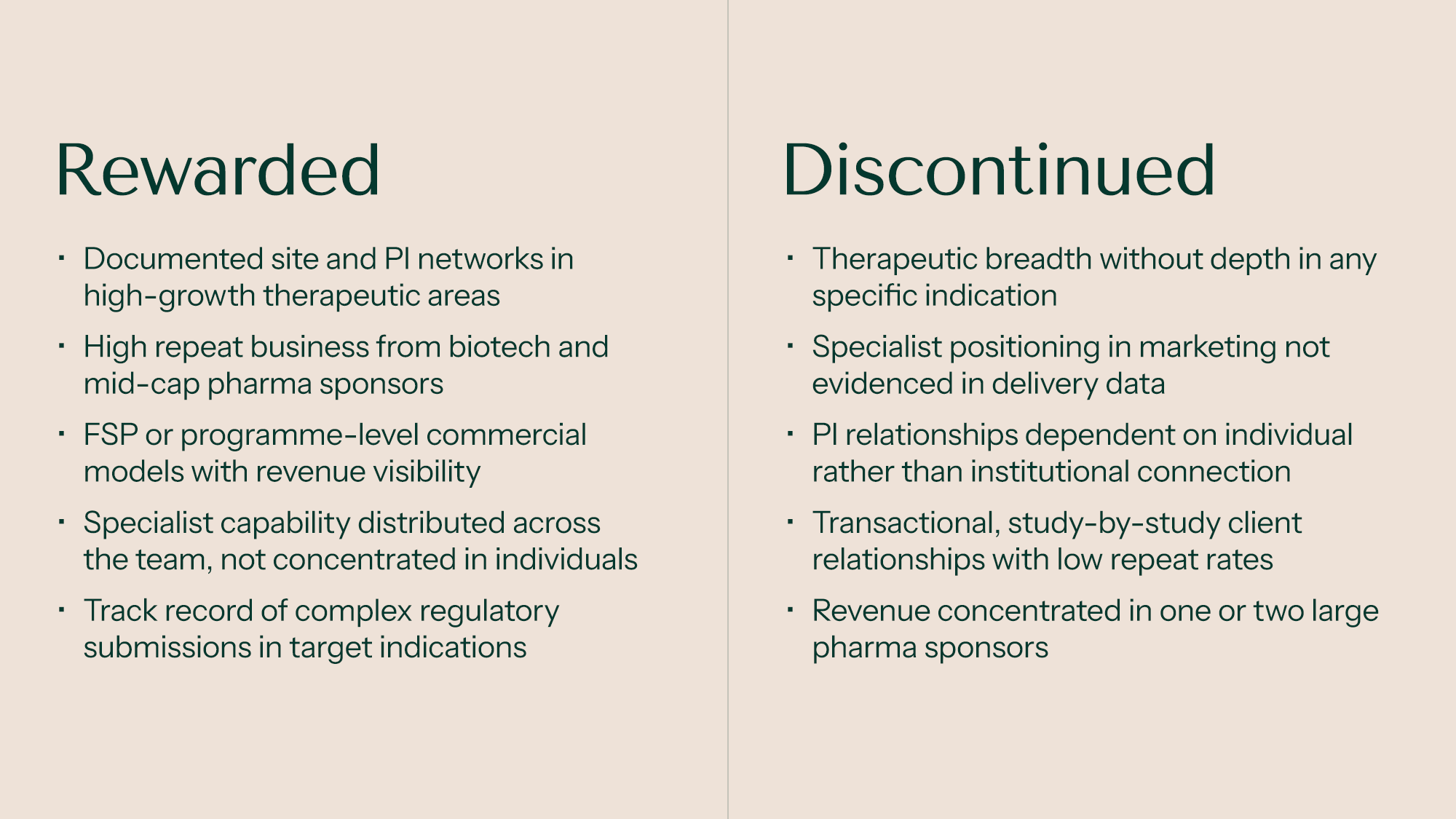

The central question acquirers are asking is whether specialist capability is embedded in the organisation or dependent on individuals. A business where oncology expertise sits with the founder or a single senior clinician carries a fundamentally different risk profile compared to one where it’s distributed across a team, documented in process, and evidenced in client relationships that extend beyond any one person. This is the first thing that comes under scrutiny and it shapes how everything else in diligence is read.

Site and PI networks are assessed through the same lens. Investigator relationships that are contractualised and transferable, and site activation times that are consistently fast in complex indications, point to institutional capability. Those that depend on personal relationships with one or two individuals do not survive the same scrutiny.

Client data tells the rest of the story. High repeat business from biotech and mid-cap pharma sponsors, programme-level or FSP commercial models with revenue visibility, and a track record of complex regulatory submissions in target indications are the markers of a business sponsors genuinely rely on. Revenue concentrated in one or two large pharma sponsors, or transactional study-by-study relationships with low repeat rates, signal the opposite, and buyers price both accordingly.

The businesses achieving the strongest multiples are those where specialisation is visible in how they operate, not just how they present themselves to the market.

Building for a premium outcome

The conditions for specialist CRO founders considering a transaction are, by most measures, favourable. Trial volume is concentrating in the therapeutic areas where specialist CROs operate, acquisition appetite is strong, and the deals being done demonstrate that buyers will pay a premium for genuine depth.

Businesses that have built their specialisation into how they operate - distributed expertise, documented networks, repeat business from sponsors who return with their most complex programmes - are achieving materially better outcomes than those where specialisation exists only in positioning.

The characteristics that command a premium in M&A are the same ones that make a business operationally strong. Building them takes time, and the window for well-positioned specialist CROs in the current market is open.

For a confidential discussion about how your business may be assessed in the current market, contact Tura’s Healthcare & Life Sciences advisory team.