Private Equity In Tech Services M&A: Pace, Scrutiny, and How To Prepare

Highlights:

Private equity is now a dominant buyer in UK tech services and its fund structure often shapes how deals are run.

The urgency and scrutiny founders experience in PE processes often stem from hold periods and fund return timelines, rather than personal intent.

In tech services, PE value creation is typically driven through growth and capability expansion, meaning how a business is positioned ahead of a sale can materially influence the outcome.

Private equity (PE) has become a defining force in technology services M&A. Over the past decade, PE investment in the global tech sector grew from $100 billion to $675 billion annually, and within that, technology services has emerged as one of the most actively targeted segments.

In the UK alone, PE is now involved in nearly eight in ten IT services transactions. Across the broader technology services landscape, the picture is similar. If you're a founder in this space, the question is no longer whether you'll encounter PE. It's whether you'll be ready when you do.

PE has a reputation that’s been built over decades of headline-grabbing buyouts, aggressive restructuring, and businesses that emerged from ownership looking very different to when they went in. Those stories are real, and it would be wrong to pretend they never happened. But they belong to a version of PE that has evolved considerably, and entering a process carrying assumptions from that era is an expensive mistake for founders to make.

Understanding how PE actually works - the mechanics, the pressures, the incentives - will make you significantly better equipped to navigate it.

The machine that drives PE buyouts

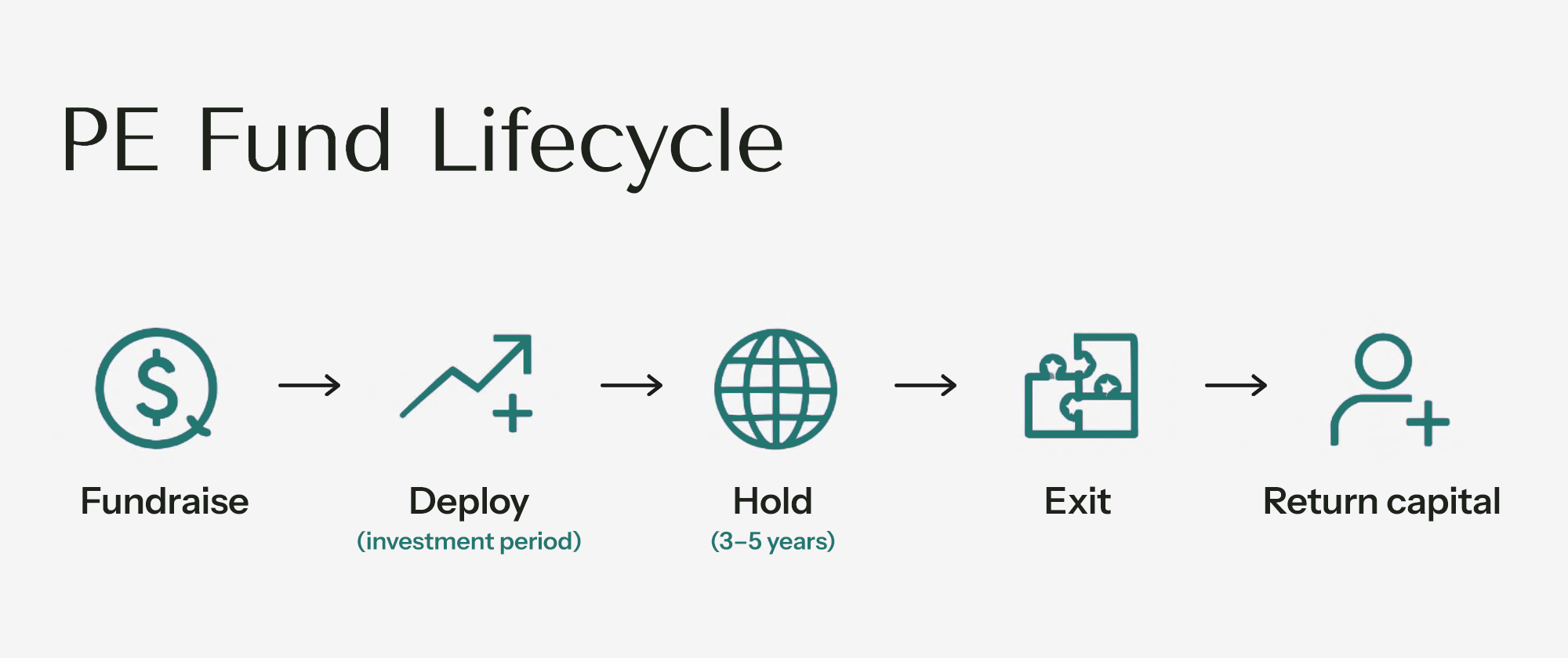

To understand why PE feels the way it does, you need to understand how PE funds are structured.

When a private equity firm raises a fund, it draws committed capital from institutional investors (pension funds, endowments, family offices) who expect that capital to be deployed and returned with a profit within a defined timeframe - typically ten years. Within that window, the PE firm must identify targets, acquire them, grow them, and exit.

The same PE firm can feel materially different depending on where it sits in that cycle. An early-cycle investor (years 1 - 5) may approach you with time to build. A late-cycle fund (years 6 - 10), may enter with a sharper focus on exit timing from the outset, and that can change the tone of the process.

During the first half of a fund’s life (its deployment period) pressure is about putting capital to work. This creates what the industry calls dry powder: committed capital that has been raised but not yet deployed. Global estimates put dry powder in private equity markets at over four trillion dollars. Sitting on this capital is not a passive position for PE firms. The institutional investors backing the fund need to see deployment, because undeployed capital earns nothing.

As a fund approaches the end of its deployment period and moves into its realisation phase, pressure intensifies. Now is the time for fund managers to start making returns for their clients (investors). Exiting becomes more critical at this stage, particularly within the final three years of realisation.

Understanding where a PE firm sits within that cycle is one of the simplest ways to gauge how pressurised the environment is likely to feel from day one.

The PE ownership timeline

The other factor worth understanding is hold period. The traditional PE model assumes ownership of three to five years before exit - enough time to implement a value creation plan, demonstrate performance improvement, and find the right moment to sell.

When macroeconomic conditions extend hold periods beyond that range - as they did during the era of higher interest rates and reduced deal activity - it creates additional pressure downstream. More assets queuing for buyers means more urgency around new acquisitions to keep the fund active and the strategy on track.

Ultimately, a PE firm’s ability to raise its next fund - often at a larger size - depends on demonstrating that it can both deploy capital effectively and generate meaningful returns. That track record is what fuels future deals.

None of this is ruthlessness for its own sake. It’s the architecture of a model designed to deliver returns on a timeline. When you're on the other side of the table, that urgency can feel personal, but it isn't. And knowing that changes how you respond to it.

What PE looks for from tech services businesses

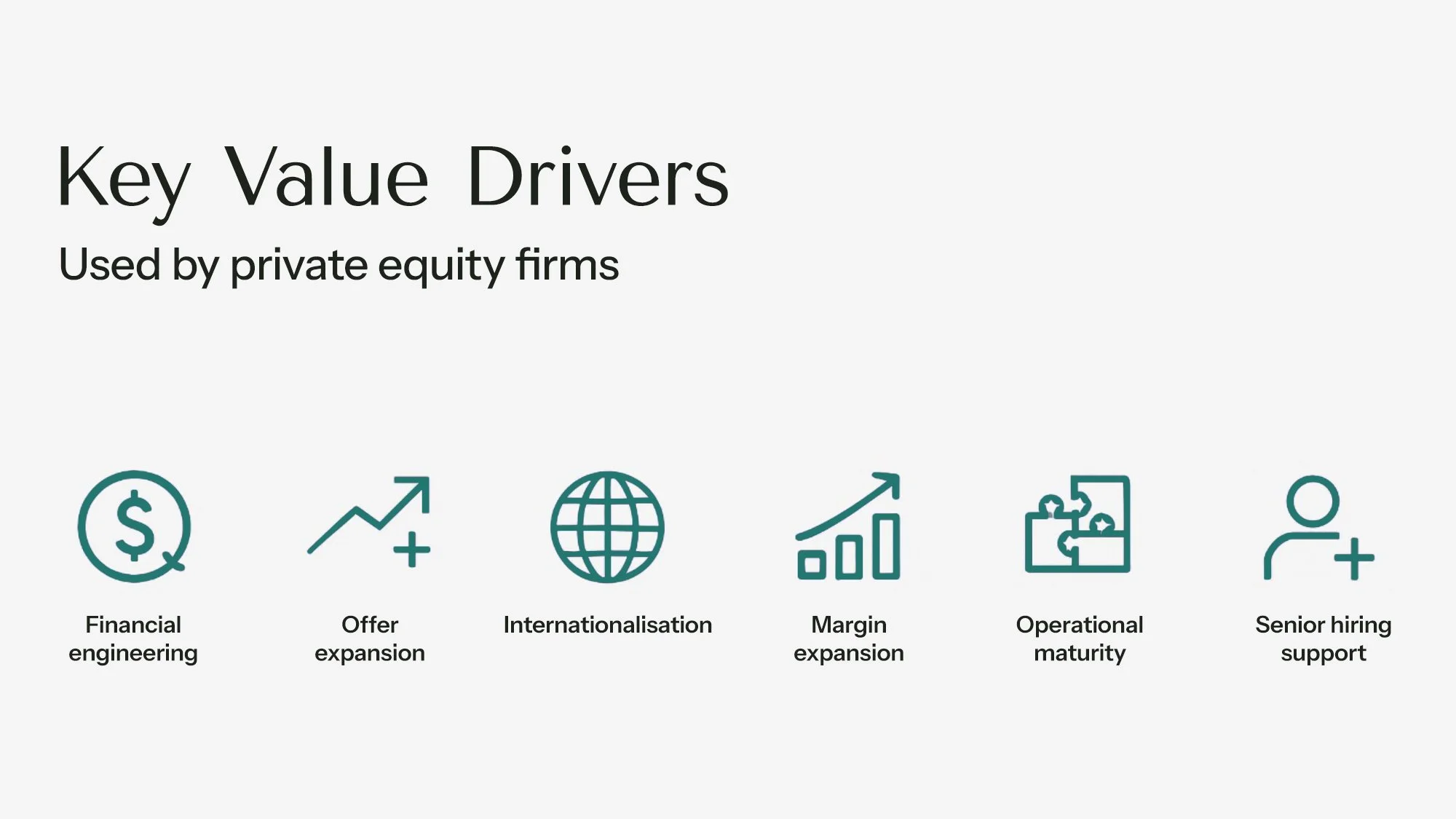

The image of PE as an extractive force that comes along and cuts costs, leverages up, then sells on was shaped by a former era of PE investment in M&A. In technology services, the value creation playbook looks quite different today than it did a decade ago.

Analysis of PE exits in the sector consistently shows that returns are driven primarily by genuine performance improvement, not debt structuring or multiple expansion alone. PE investors need portfolio companies to actually grow - to win new clients, deepen specialisation, retain key people, and develop their service capabilities. A firm that hollows out a tech services business in pursuit of short-term margin doesn't generate the returns its investors need.

The incentive structure, in tech services at least, points towards building rather than extracting. The businesses that have delivered the strongest outcomes under PE ownership in this sector share a clear pattern: they scaled well-defined competencies, shifted towards higher-value digital services, and were led by founders or management teams who remained entrepreneurial and customer-focused throughout the hold period.

Wavenet is a useful example. When Beech Tree Private Equity invested in 2016, the business had a £14m turnover and a clear position as both an internet service provider and managed service provider. Rather than sweating that existing base for margin, Beech Tree backed eight acquisitions targeted at building out connectivity, cloud and cyber capabilities - the higher-value services that enterprise clients were increasingly demanding.

By the time Beech Tree exited to Macquarie Capital in 2021, revenue had grown to over £60m and EBITDA had increased fivefold. The strategy throughout was additive, not extractive. Macquarie then continued that same trajectory, ultimately culminating in a merger with Daisy Corporate Services to create the UK's largest independent IT managed services provider.

A similar pattern can be seen in data-led technology services. Baird Capital’s minority investment in JMAN Group was positioned around scaling its consulting, data science and engineering capabilities, alongside international expansion into North America. The investment case centred on scaling capability and geographic reach, not short-term extraction.

As a founder, it's important to understand that the qualities that built your business - the relationships, the instincts, the drive - are not incidental to what PE needs. In technology services, they are often central to the returns thesis.

This isn’t an argument that every PE firm is a good actor, or that all processes are well-run. It’s an argument that the incentives are better aligned than the reputation suggests, and that understanding those incentives gives you a far clearer lens through which to evaluate what you're being asked and by whom.

Going into PE deals with your eyes open

The commercial pressure of a PE process doesn't disappear once you understand where it comes from. PE is fast, scrutinous, and structured around outcomes that are ultimately defined by the fund's needs. Due diligence is forensic. Timelines are real. The people across the table are professionals whose job is to transact on the best possible terms for their investors.

But there is a meaningful difference between a founder who enters that environment with clarity and one who enters it carrying unexamined fears.

The first can read urgency accurately and distinguish genuine deal momentum from manufactured pressure tactics. They can assess what's being asked of them in due diligence, what's standard, and where their position is stronger than they might feel in the moment. They can have more honest conversations about what the hold period will look like, what the exit thesis means for their team and their culture, and what kind of PE partner actually fits the business they've built.

The second walks in disadvantaged before the first conversation has happened.

Tura works with founders across the full spectrum of technology services M&A, and the conversations we have before a process begins matter as much as the ones we have during it.

PE is not an enemy. It’s a specific type of capital, operating within specific constraints, in pursuit of specific outcomes. The founders who navigate it most effectively are those who understand those constraints as clearly as the people deploying the capital do.

Whether you’re planning ahead or actively exploring a private equity sale, we’ll guide you through your options with clear, strategic advice and complete confidentiality. Schedule a consultation here.